Tiếng Việt

Tiếng Việt

English

English

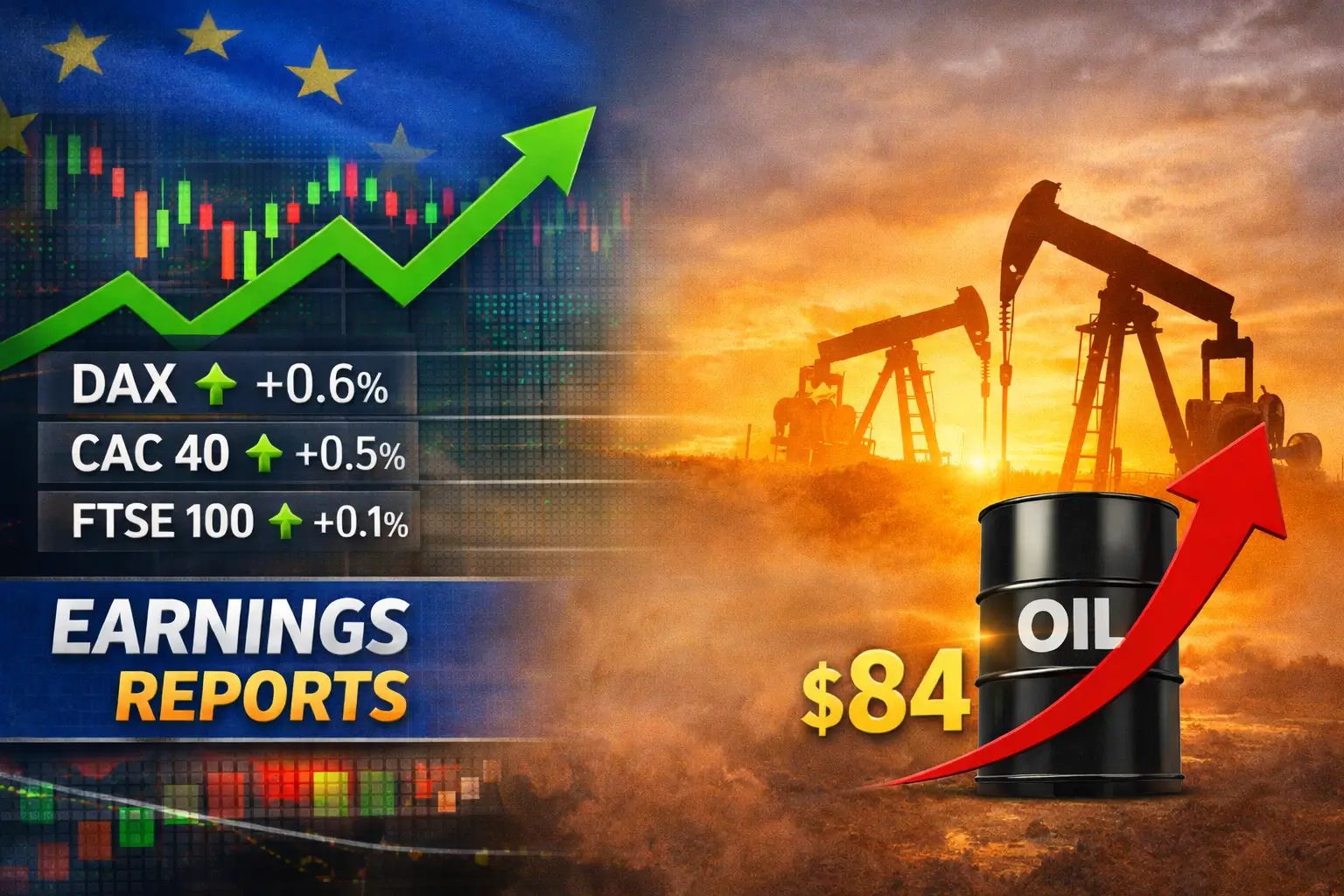

European equity markets posted modest gains on Wednesday, as investors balanced escalating geopolitical tensions in the Middle East against a steady flow of corporate earnings updates.

European equity markets posted modest gains on Wednesday, as investors balanced escalating geopolitical tensions in the Middle East against a steady flow of corporate earnings updates.

As of 3:05 p.m. Hanoi time, Germany’s DAX rose 0.6%, France’s CAC 40 gained 0.5%, and the UK’s FTSE 100 added 0.1%.

The cautious advance reflects a market attempting to stabilize amid intensifying geopolitical developments and persistent inflationary pressures linked to surging energy prices.

Overnight, U.S. and Israeli forces carried out additional strikes on Iranian targets, further intensifying the regional conflict. U.S. Admiral Brad Cooper, commander of American forces in the Middle East, stated that Iran’s air defense systems had been significantly degraded. He also claimed that Iran’s navy had lost operational capacity along major waterways after 17 vessels were sunk and that more than 2,000 Iranian targets had been hit.

Israel simultaneously expanded operations against Hezbollah forces in neighboring Lebanon, following retaliatory gunfire after the death of Iran’s Supreme Leader in initial strikes over the weekend.

Iran responded by launching missiles and drones at neighboring Arab countries hosting U.S. military bases, widening the conflict across the region.

Analysts at Vital Knowledge noted that energy prices—particularly European natural gas—have surged sharply in recent days. This dynamic has weakened the traditional role of bonds and yields as a “circuit breaker” for equities. If elevated energy prices persist, they could become a major headwind for consumers worldwide.

Still, some market observers suggest that beyond the immediate turmoil, there is potential for longer-term stability if the campaign ultimately brings an end to a broader conflict that began in 2023.

Beyond geopolitical risks, investors are closely monitoring the ongoing earnings season, with several major European companies reporting results on Wednesday.

German pharmaceutical giant Bayer issued a 2026 earnings outlook below market expectations, as the company continues to grapple with costly litigation and a heavy debt burden.

Automotive supplier Continental AG projected broadly stable 2026 sales and profit guidance for its core tire division, amid fluctuating global demand.

In a more positive development, sportswear manufacturer Adidas said it expects operating profit to rise to around €2.3 billion this year, despite facing an estimated €400 million hit from U.S. tariffs and adverse currency movements.

In the financial sector, French reinsurer SCOR reported fourth-quarter net income that exceeded expectations, driven by strong underwriting performance in both property & casualty and life & health segments.

Meanwhile, UK-based Metro Bank posted underlying pre-tax profit of £98 million for the 2025 financial year—the highest in its 15-year history—while also surpassing cost-cutting guidance.

On the downside, Traton, the truck-making subsidiary of Volkswagen, proposed a dividend nearly half of the previous year’s level after reporting a sharp drop in earnings. The decline was attributed to a near-collapse in North American operations and rising costs linked to U.S. tariffs.

Investors are also awaiting key economic data, including February services PMI figures and the latest unemployment numbers for the Eurozone.

However, these releases are unlikely to significantly shift expectations for the European Central Bank, particularly after Tuesday’s data showed an unexpected rise in inflation.

Inflation across the 21 euro-area countries climbed to 1.9% last month, up from 1.7% previously and above market forecasts. If energy prices remain elevated due to ongoing conflict, inflationary pressures could intensify in the coming months.

Financial markets currently expect the ECB to keep its deposit rate unchanged at 2%. Nevertheless, the probability of a rate hike later this year has increased as inflation risks resurface.

Energy markets remain at the center of investor attention. Oil prices continued to climb on Wednesday, extending recent gains amid fears of supply disruptions stemming from the Middle East conflict.

Futures for Brent crude jumped 2.9% to $83.78 per barrel, while U.S. West Texas Intermediate (WTI) crude rose 2.6% to $76.51 per barrel.

Both benchmarks had already gained nearly 5% in the previous session, adding to Monday’s 7% surge. Brent is now trading at its highest level since July 2024.

According to Reuters, Iraq—OPEC’s second-largest crude producer—has cut output by nearly 1.5 million barrels per day, roughly half of its production capacity, due to storage constraints and limited export routes.

Meanwhile, Iran has reportedly targeted oil tankers transiting the Strait of Hormuz, a critical chokepoint through which around one-fifth of global oil and liquefied natural gas flows. Traffic through the strait has effectively been disrupted for a fourth consecutive day.

The combination of geopolitical uncertainty, rising energy costs, and ongoing earnings updates leaves European markets in a delicate balancing act.

In the near term, market direction will likely hinge on:

Further developments in the Middle East conflict

The trajectory of oil and gas prices

Signals from the ECB regarding monetary policy

The sustainability of corporate earnings momentum

While European stocks remain in positive territory, the foundation appears increasingly fragile as elevated energy prices threaten consumer spending and corporate profitability.

European equities edged higher on Wednesday, reflecting cautious optimism amid a highly uncertain backdrop. Escalating tensions in the Middle East and surging oil prices are emerging as key variables that could reshape inflation expectations and monetary policy outlooks.

For now, markets are holding steady. But as energy volatility intensifies and geopolitical risks persist, investors may need to brace for heightened fluctuations across both equity and commodity markets in the weeks ahead.